Last updated: July 09 2013

Re-Accumulation: Thinking It Through

Don's incredulous. He’s a do-it-yourself investor and he has had a bad several years. His half a million dollar RRSP portfolio is now worth $250,000. He wants to know: What does it take to recover and re-accumulate $250,000 over the next ten years—the time Don has left until retirement?

Simple math would tell you that's $25,000 in new savings every year, and that's a lot of new money to save—impossible for most, unless a lottery or inheritance suddenly falls out of the sky. So, realistically, what can be done?

At one point Don had decided to "stop the bleeding" and sold his stocks in his registered portfolio. Now he's looking at safer fixed income investments to recover his losses. Trouble is, with a 50% decrease in value, he'll need a 100% increase in his remaining capital just to get back to square one—and that's not even taking into account that inflation will have eroded the purchasing power of his savings during the recovery process.

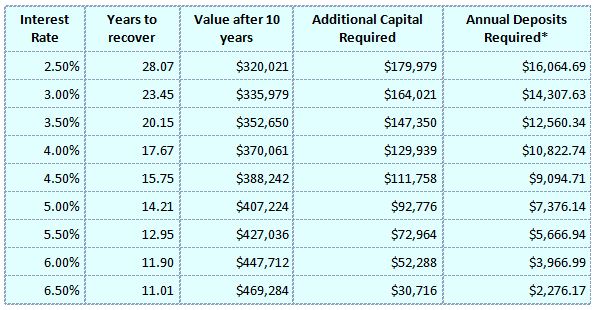

Let's take a look at recovery times at various income levels and how much additional capital will be required to recover within Don's 10-year window. See the following table. These calculations assume that the savings are in a registered account so that the earnings are not eroded by income tax.

For non-registered accounts, to adjust for taxes, use an interest rate that is equal to the actual rate x (1 - MTR). Thus, for example, if you invest at 5% and your marginal tax rate is 40%, the equivalent yield is 5% x (1 - 0.4) = 3%.

* Assumes deposits are made at the end of the year.

So, if Don were to invest the entire $250,000 in 10-year government bonds, which are currently yielding 3.17%, his saving would have recovered to $341,566 at the end of 10 years. In order to make it back to $500,000 before retirement, Don would have to add an additional $13,712 to the pot each year. He should also keep in mind that, depending on inflation rates over the next ten years, $500,000 could have a purchasing power of less than what $400,000 has today.

What would you advise Don to do? Here’s our checklist:

Tax Tips on Short Term, Tax Efficient Recoveries

- Make RRSP contributions

- Make TFSA contributions (January 1)

- Reduce tax withholding and the December 15 instalment payment

- Increase this year's tax refund: dig for every tax deduction and credit you are entitled to

- Transfer winning stock from non-registered portfolios: make charitable donations before year end

- Carry losses on non-registered investments back to offset taxes paid on previously reported capital gains

- Buy assets before year end to increase deduction for Capital Cost Allowances

- Reduce mortgage interest and credit card payments, invest savings

- Take a second job or consulting contract

- Rent out a room in the house

- Stop feeding the kids cheese. . .